The repo rate vs prime lending rate? Which one should I be watching when calculating my home loan repayments?

|Published

Changes in the prime lending rate are dictated by adjustments in the repo rate and home owners should understand how they affect their bond repayments.

Durban – Home owners and buyers are continually being urged to manage their budgets, especially as interest rates are on the increase.

But for many who eagerly watch the interest rate changes following the Monetary Police Committee’s meetings every second month, there may be some confusion with which rates they should actually be focusing on.

Is it the repo rate that South African Reserve Bank (SARB) Governor Lesetja Kganyago talks about in his addresses, or the prime lending rate that banks and economists use to explain how home loan repayments will be affected? How are they related, and which will ultimately help home owners plan their bond repayments?

The technical answer is both, as the repo rate – the rate at which the SARB lends money to the commercial banks – dictates the prime lending rate – the rate that consumers are charged when borrowing money. But as FNB property economist John Loos explains, home owners can make their lives easier by just monitoring the latter.

“The prime lending rates of the major banks are almost always set at 3.5% above the repo rate. It does not have to be this way but has been for over 20 years. So when the repo rate goes up or down, the prime lending rate, which in turn affects consumers directly, does too.”

There is a few days’ lag between the repo rate adjustments and the corresponding adjustments in prime by commercial banks, he adds.

“As a home owner you can watch both rates in tandem, but your home loan repayment will ultimately be affected by the change in your bank’s prime lending rate, if your floating interest rate is linked to prime.”

Read our latest Property360 digital magazine below

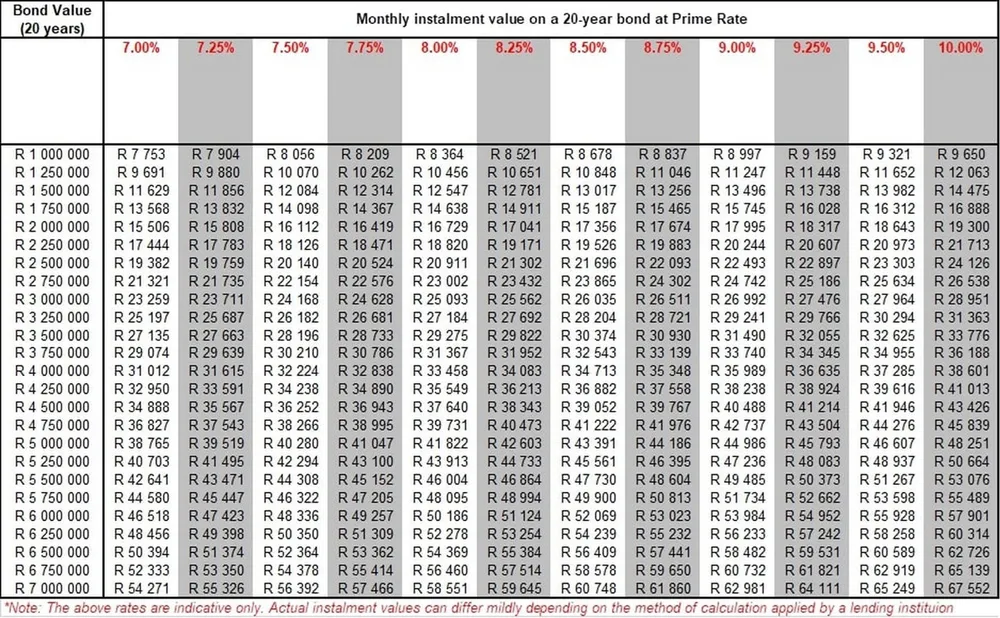

The current prime lending rate is 7.75%, and FNB predicts that this rate will increase by 0.25% after each of the four MPC meetings left this year. This will ultimately make the prime lending rate 8.75% by the end of this year.

To break it down for home owners, Loos says that the bond repayment on a R1 million home is currently R8 209, but by the end of the year, based on a prime lending rate of 8.75%, this will increase to R8 837 – meaning home owners will be paying R628 more than they are paying now.

On a new 20-year R2m home loan at prime lending rate, consumers currently paying R16 419 a month will pay an extra R1 255 a month by the end of this year, taking their repayments to R17 674, should the prime rate indeed rise to 8.75%.

FNB then expects the interest rate to stabilise next year at 9.25%. This would mean that home owners of a R1 million home could be paying R9 159 on their bond each month at the end of 2023, an increase of R950 a month from what they are paying now on a new 20-year home loan at prime rate.

Owners of a R2m home could pay R18 317 by the end of 2023, an extra R1 898 a month, compared to what they are paying now on a new prime rate loan, should FNB’s forecast materialise.

“We also expect, in the current interest rate cycle, that the prime lending rate will remain at 9.25% at the end of 2024.”

To assist home owners with their planning, Loos prepared the following table to allow them to calculate what they are likely to pay at different interest rates over the next three years.

He emphasises, however, that these figures are indicative, and that there may be slight differences between this table and actual home loan payments depending on how a home owner’s bank calculates the effective interest rate.

Now that you have an idea of what to expect from the interest rates over the next three years, start your search for your new home here.

IOL WEALTH