The Supreme Court of Appeal found that SARS had fundamentally changed the factual basis of its case after issuing the original tax assessment

Image: Timothy Bernard | Independent Newspapers

The Supreme Court of Appeal has dismissed an attempt by the Commissioner of the South African Revenue Service (SARS) to revive a R183.5 million tax claim linked to a complex series of share transactions tied to the Steinhoff–Pepkor deal, after finding the tax authority unlawfully changed the basis of its case during litigation.

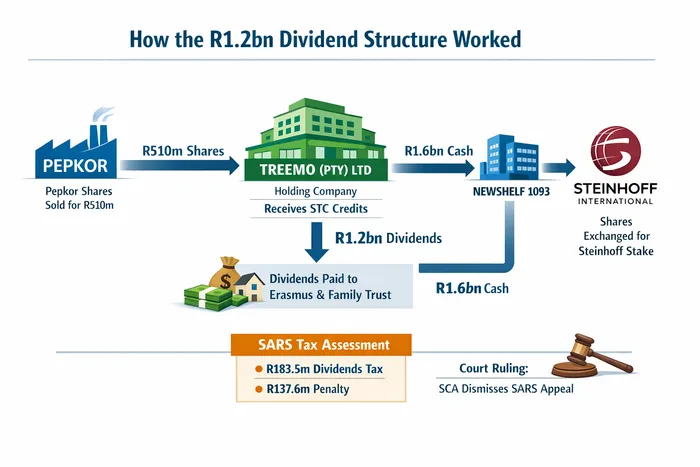

The dispute centres on more than R1.2 billion in dividends paid to businessman Pieter Johan Erasmus by Treemo about a decade ago, which SARS said formed part of an impermissible tax avoidance arrangement.

The case stems from a restructuring of Erasmus’s assets as Pepkor shareholders prepared to exchange their shares for shares in Steinhoff International Holdings.

Steinhoff International was liquidated after it emerged that corporate fraud amounting to about €6.5 billion, roughly R134 billion, had been described as accounting irregularities. The Public Investment Corporation lost close to R21 billion in investments linked to the group.

The irregularities, leading to the Steinhoff collapse being called the largest corporate scandal as of 2025, were unearthed by Deloitte in 2017, which resulted in Steinhoff’s shares collapsing.

As part of the restructuring, Erasmus transferred assets including Pepkor shares to Treemo in exchange for shares in the company, consolidating his holdings into a single structure.

In a related transaction, shares that had been transferred to Treemo in Newshelf 1093 were later repurchased by Newshelf, generating proceeds of about R1.6 billion.

Treemo subsequently used those proceeds to subscribe for new shares in Newshelf, which were ultimately exchanged for shares in Steinhoff as part of the Pepkor transaction.

SARS argued the structure amounted to an impermissible avoidance arrangement designed to use secondary tax on companies credits to shield dividends from tax.

The tax authority issued a dividends tax assessment of R183.5 million against Erasmus, along with an understatement penalty of R137.6 million and interest.

Erasmus challenged the assessment in the Tax Court after SARS filed a statement opposing his appeal that introduced a different factual explanation for the alleged tax avoidance arrangement.

The Tax Court set the filing aside as an irregular step. SARS then appealed the ruling to the Supreme Court of Appeal.

In its judgment, the appeal court dismissed SARS’ appeal and ordered it to pay Erasmus’s legal costs, including the costs of two counsel.

The court found that SARS had fundamentally changed the factual basis of its case after issuing the original tax assessment.

Initially, SARS argued that the dividends paid to Erasmus were funded by proceeds from the Newshelf share repurchase.

The confusing R1.2 billion dividend structure.

Image: ChatGPT

However, when filing its statement opposing the taxpayer’s appeal, SARS abandoned that explanation and instead relied on a different set of transactions involving a share subscription by Erasmus’s trust and a call option arrangement linked to Treemo shares.

Judge Keightley said the change went to the core of the tax authority’s case.

“In effect, they amount to a new exercise of that power without the requisite prior legal steps having been followed,” the court said.

SARS defended the amendment, saying it changed its position after seeing a Treemo bank statement dated 27 March 2015 showing a payment of R1.39 billion from the trust for the subscription of new shares.

“Although these annual financial statements had been provided previously to the Commissioner, it was only when the taxpayer drew his attention to note 5, and provided the bank statement, explained the Commissioner, that he had accepted the taxpayer’s explanation of the source of funds for the payment of the dividends,” the judgment stated.

This, stated the Commissioner, “was the first concrete and independent evidence to support the taxpayer’s explanation. It was this that led to the modification and amendment,” the ruling said.

However, the court held that SARS could not rely on provisions of the Income Tax Act or procedural rules governing tax appeals to alter the factual basis of the assessment after it had been issued.

Because SARS had changed both the factual basis of the alleged avoidance arrangement and the remedy it sought to impose, the court found the changes effectively required a new tax assessment.

SARS was ordered to pay Erasmus’s legal costs, including the costs of two counsel.

IOL BUSINESS